Navigating modern retirement requires a multifaceted approach, especially during an era of greater market volatility, recession fears, and inflation pressures. According to the recent Charles Schwab 401(k) Participant Survey, 62% of workers now see inflation as a formidable barrier to achieving a secure retirement—a significant surge from last year (42%).

Amidst the challenges of a volatile economic landscape and the reality of longer life expectancies, employees planning for retirement need more than just a 401(k); they need a comprehensive, forward-thinking strategy. Employers play a critical role in equipping their employees with the tools and information needed to confidently navigate their retirement journeys.

This article covers an in-depth explanation of the 401(k) and its role in the job market, related legislative changes like the Setting Every Community Up for Retirement Enhancement Act of 2022 (“SECURE 2.0 Act”), and holistic financial benefit recommendations beyond the 401(k) to support employees in planning for a successful retirement.

Pressed for time? Here’s a quick summary…

- The Significance Of The 401(k): A 401(k) is a “must-have” for 9 in 10 job seekers, emphasizing the significance of providing robust retirement benefits to attract and retain top talent.

- SECURE 2.0 & Legislative Shifts: SECURE 2.0 aims requires automatic enrollment in 401(k) plans, increases catch-up contributions, and expands access to retirement savings for part-time workers. Employers need to help employees understand the key provisions of the law so that they can take advantage of the changes.

- Financial Education & Planning: Offering education and access to advisors can enhance employees’ financial well-being and literacy. A personalized approach that leverages both human expertise and artificial intelligence is optimal for balancing employee preferences with technological advancements.

- Tax-Advantaged Accounts: Tax-advantaged accounts such as Health Savings Accounts, Flexible Spending Accounts, and 529 plans can boost employees’ savings by enabling them to use pre-tax income for eligible health or educational expenses.

What Is A 401(k)?

A 401(k) is an employer-sponsored savings plan that allows employees to set aside a portion of their earnings to save for their retirement.

There are two main types of 401(k) plans:

- Traditional 401(k): Individuals invest pre-tax dollars, reducing current taxable income.

- Roth 401(k): Individuals invest after-tax dollars, offering tax-free withdrawals during retirement.

Tax Implications

Traditional 401(k) contributions grow tax-deferred, meaning individuals are taxed only upon withdrawal in retirement when their tax bracket may be lower.

Limits & Contributions

401(k) plans come with annual contribution limits set by the IRS. The contribution increase for 2024 is projected to be $500, creating a top contribution level of $23,000. Employers often offer matching contributions, effectively boosting individuals’ retirement funds.

Vesting is an important concept within a 401(k) plan that determines an employee’s ownership rights to the employer-contributed funds in their retirement account. When an employer offers a matching contribution to an employee’s 401(k), these funds may not immediately belong to the employee. Instead, vesting sets a specific period during which an employee gradually gains full ownership of these contributed funds.

Hardship Withdrawals & Loans

Although primarily designed for retirement, 401(k)s allow hardship withdrawals or loans in dire situations. However, this can impact individuals’ long-term savings goals and may lead to penalties or taxes.

What Is A 401(k)’s Role In The Job Market?

The 401(k) has become an integral part of any successful employee benefits package, now considered a non-negotiable advantage by job seekers:

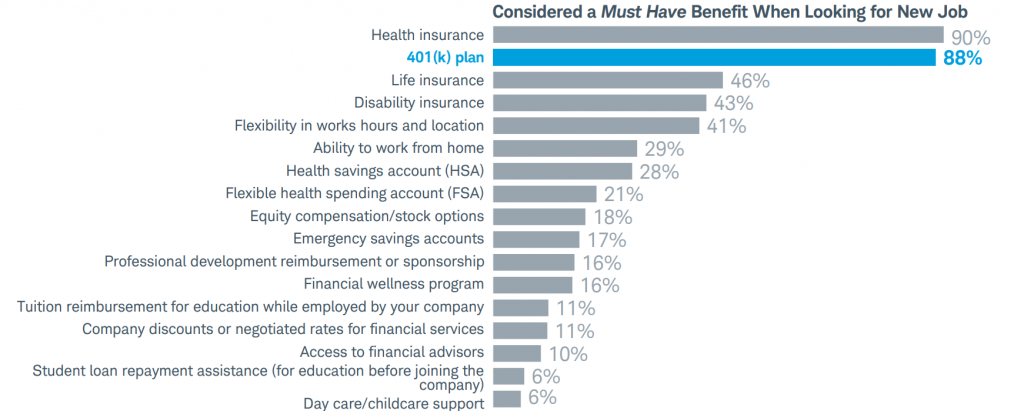

- Nearly 9 in 10 job hunters consider a 401(k) a “must-have”.

- 3 in 4 would turn down a job lacking a 401(k) plan.

This holds profound implications for employers aiming to attract top talent.

Driving Employee Retention

A robust 401(k) plan is a powerful tool for fostering employee loyalty and curbing turnover. 71% of US employees say they are more likely to stay with an employer that provides an employer-sponsored retirement savings plan, a notable increase from the 60% reported in 2022.

Attracting A Diverse Workforce

The allure of a comprehensive 401(k) resonates across a diverse range of candidates, from fresh graduates to seasoned professionals. Tailoring 401(k) benefits can amplify a company’s inclusivity, broadening its appeal to a wider demographic.

The Global Context

The US 401(k) stands out as a distinctive model with advantages that set it apart from other global retirement savings systems.

- Flexibility: The US 401(k) system distinguishes itself by enabling individuals to customize their retirement savings strategies, aligning investments with personal risk preferences and financial objectives.

- Tax Advantages: Unlike many global counterparts, the 401(k) system’s pre-tax contributions and potential employer matches provide significant tax benefits, promoting accelerated growth of retirement funds.

- Portability: US 401(k) accounts are often portable, allowing workers to carry their retirement savings when changing jobs without complex account transfers.

- Individual Responsibility: The 401(k) system places a higher degree of responsibility on individuals to manage their retirement savings effectively, promoting greater control over investments but necessitating financial literacy and engagement.

Steering Retirement Plans Through Legislative Waters: SECURE 2.0

Employers play a pivotal role in keeping their workforce informed about the retirement implications of legislative changes, particularly the SECURE 2.0 Act. This act expands retirement plan coverage, aiming to enhance retirement readiness among workers. SECURE 2.0 outlines both required and optional changes to defined contribution plans, including:

- Qualified Student Loan Payments: Plan sponsors have the option to consider qualified student loan payments as eligible for employer matching contributions. These payments cannot exceed the maximum annual deferral limit under a 401(k), minus the employee’s elective deferrals for the year.

- Pension-Linked Emergency Savings Accounts (ESAs): DC plans can now incorporate ESAs. Non-highly compensated employees may contribute on a Roth basis, with contributions limited to $2,500 (indexed for inflation) or a value designated by the plan sponsor.

- Roth Catch-Up Contributions: Plans offering catch-up contributions must mandate Roth catch-up contributions for participants with prior-year wages exceeding $145,000 (indexed for inflation).

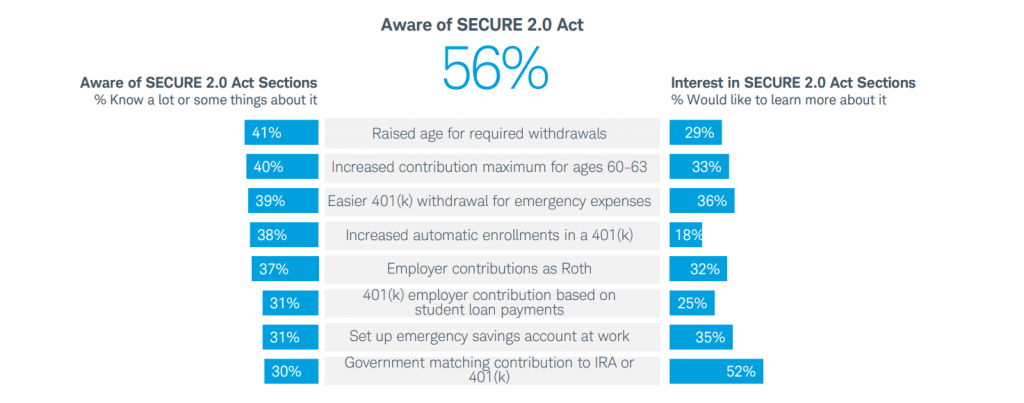

Just over half of workers are already aware of SECURE 2.0. Among the various sections within the act, they are most familiar with those regarding required minimum distributions (RMDs) and expanded catch-up contributions. RMDs refer to the minimum amounts retirees must withdraw from their retirement accounts annually after reaching a certain age, while expanded catch-up contributions allow older savers to contribute additional amounts to their retirement accounts beyond the usual limits.

Nevertheless, a significant portion of employees are still unfamiliar with the act or want to learn more about it. By offering guidance on legislative shifts like SECURE 2.0, employers can empower their workforce to make informed decisions, optimize their retirement strategies, and in turn, foster higher engagement and loyalty.

Exploring Holistic Benefits Beyond 401(k)s

While the 401(k) remains an indispensable pillar of retirement planning, US employees are also seeking education and holistic benefits. 60% of 401(k) savers would trade a portion of their next raise for enhanced benefits, illustrating that the pursuit of comprehensive financial wellness benefit plans is a growing priority.

Financial Wellness Education

78% of survey respondents acknowledge that current economic conditions are molding their saving habits. The implications of inflation, fluctuating markets, and economic uncertainty make financial education paramount for informed decision-making.

Employers can take several proactive steps to inform and educate employees on financial literacy, particularly in the realm of retirement planning and benefits.

- Regular Communication: Establish a regular communication channel to share financial insights and updates about legislative changes. This could include emails, newsletters, or internal messaging platforms.

- Educational Workshops: Organize workshops that cover budgeting, debt management, investment strategies, and more. By incorporating the implications of legislative changes, employees gain a more comprehensive understanding of their financial landscape.

- Webinars: Invite financial experts or specialists to conduct webinars, adding credibility and depth to financial education. Webinars are convenient, accessible, and allow employees to engage directly with professionals.

- Clear Documentation: Provide employees with easily digestible documentation—such as FAQs, guides, and fact sheets—to simplify legislative changes and general financial guidance, as complex financial jargon can often be daunting.

- Interactive Tools: Offer digital tools like online calculators or retirement planning platforms that incorporate new legislative changes into their calculations. These interactive tools allow employees to model various scenarios, making it easier for them to conceptualize the impact of legislative changes alongside their holistic financial picture.

Personalized Financial Planning

Employees are continuously seeking ways to optimize their finances. 68% of workers are choosing savings accounts to save for retirement, up from 61% last year, and 47% are opting to invest in IRAs, up from 33% last year. A one-size-fits-all approach to retirement savings no longer suffices; the intricacy of financial ecosystems calls for a personalized, diversified approach.

Providing access to financial advisors can enhance employees’ financial wellness and literacy. With expert support, employees can navigate financial complexities and make informed choices that align with their goals. This guidance is especially valuable in terms of optimizing retirement savings and 401(k) strategies.

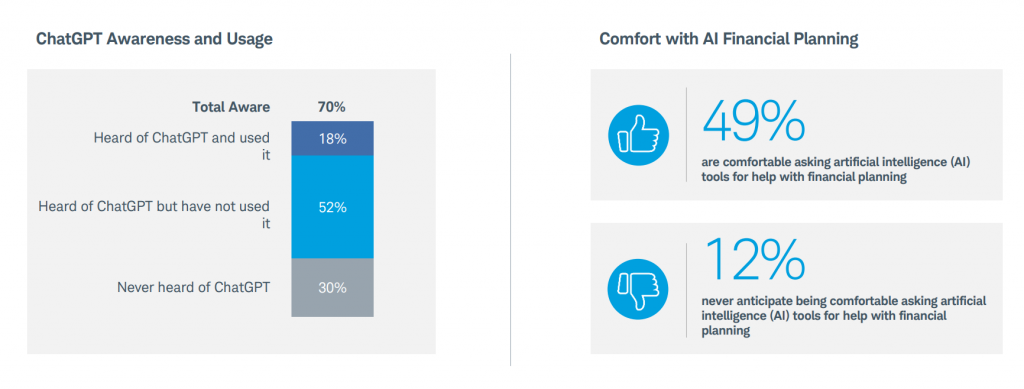

Despite the rise of artificial intelligence (AI) across various sectors, a preference for human advisors persists. While half of workers would feel comfortable asking AI tools like ChatGPT for financial planning advice, actual adoption is minimal (4%).

Workers favor human advice (95%) over computer-generated alternatives (74%), underscoring the value of human guidance for financial decision-making. A hybrid model, leveraging both human expertise and technological advancements, stands as a promising way forward.

Other Tax-Advantaged Accounts

Beyond conventional retirement planning, tax-advantaged accounts have the potential to significantly boost employees’ savings. By enabling them to use pre-tax income for eligible health or educational expenses, these accounts offer a way to bypass tax payments entirely:

- Health Savings Accounts (HSAs): HSAs offer a dual advantage of healthcare funding and retirement investment. With tax benefits, flexible usage, and potential for investment growth, HSAs are an attractive avenue for bolstering financial wellness. HSA contribution limits have risen this year in response to recent inflation.

- Flexible Spending Accounts (FSAs): FSAs allow individuals to set aside pre-tax dollars for medical expenses, enabling them to save on taxes while managing their healthcare costs efficiently. FSAs cover a wide range of eligible medical expenses, making them a practical choice for budgeting healthcare needs.

- 529 Plans: 529 plans allow parents to save money for their child’s education and grow contributions over time. When college comes around, these funds can be withdrawn tax-free, ensuring peace of mind for the parent and a solid foundation for the child’s academic journey.